- 25/03/2026

- Posted by: Janick Pettit

- Categories: Articles, Automotive, SagaCube

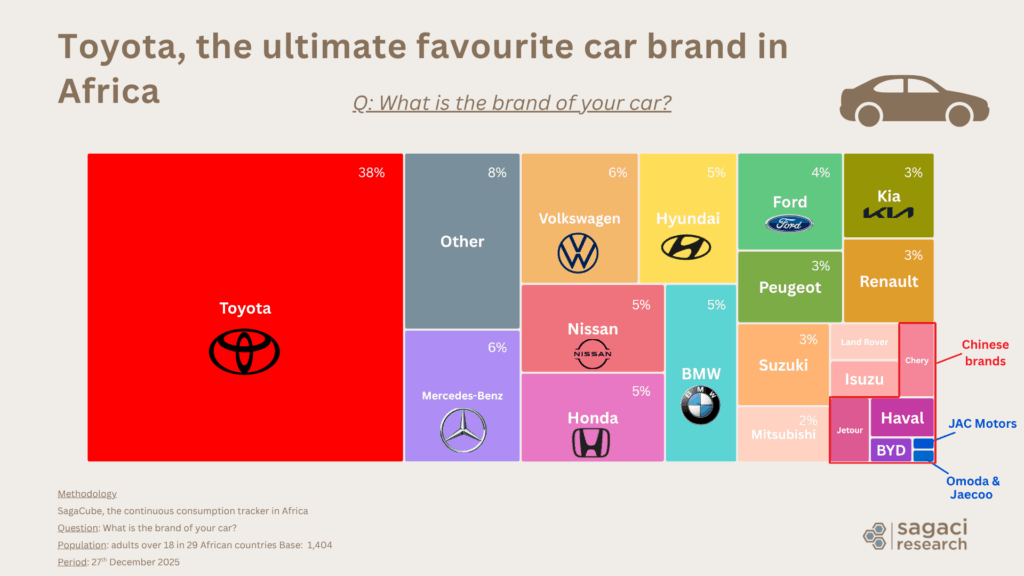

A year ago, we published our first deep dive into the car market in Africa, revealing Toyota’s commanding dominance across the continent and the wide disparities in car ownership from one country to the next. Twelve months on, we’re back with fresh data from SagaCube, Sagaci Research’s continuous consumer tracker, covering over 8,000 adults across 29 African countries.

Two findings in particular stand out: the growing openness toward Chinese car brands, and a significant shift in consumer intent toward hybrid vehicles.

Here is what the data tells us about where Africa’s car market is heading.

Car ownership in Africa: a slight dip, but structural patterns hold

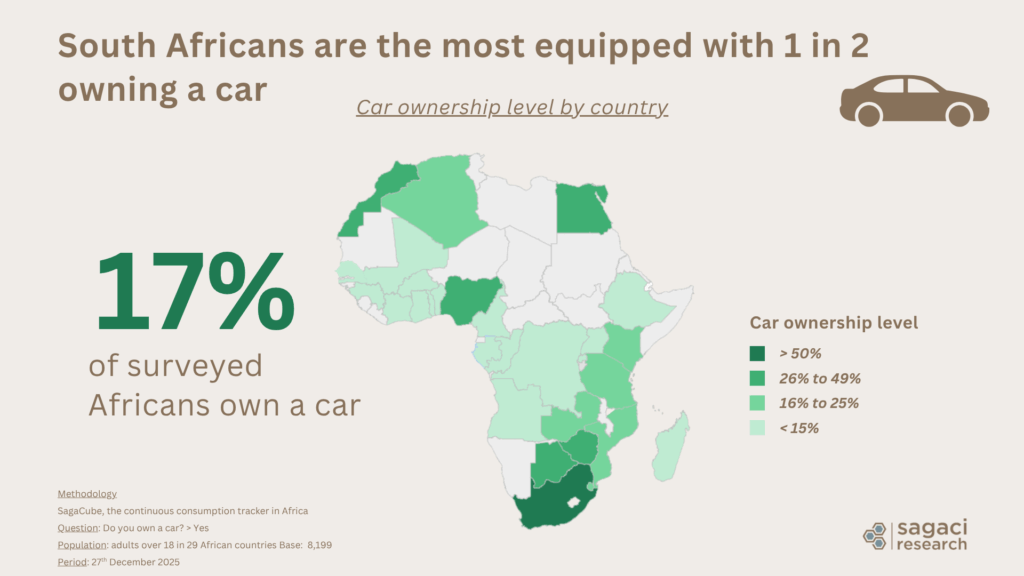

In early 2025, we reported that just under 1 in 4 Africans (22%) owned a car. Our latest wave, fielded in December 2025, puts that figure at 17% across the 29 countries surveyed. While a direct comparison requires caution given slight differences in methodology, the broader picture remains consistent. Car ownership in Africa is concentrated among older, wealthier consumers, with minimal difference between men and women.

The age and income gradients are particularly clear. Ownership rises steadily from 7% among 18 to 25-year-olds to 41% among those aged 55 and above. By socio-economic group, 44% of SEC A consumers own a car, compared to just 5% in the lowest income brackets. South Africa continues to stand out with the highest ownership rate on the continent, with 1 in 2 adults owning a car.

These structural patterns have a direct implication for automotive players. The addressable market for new cars remains narrow, which makes understanding that segment’s preferences and purchase intentions all the more important.

Chinese car brands: from curiosity to a credible competitive threat

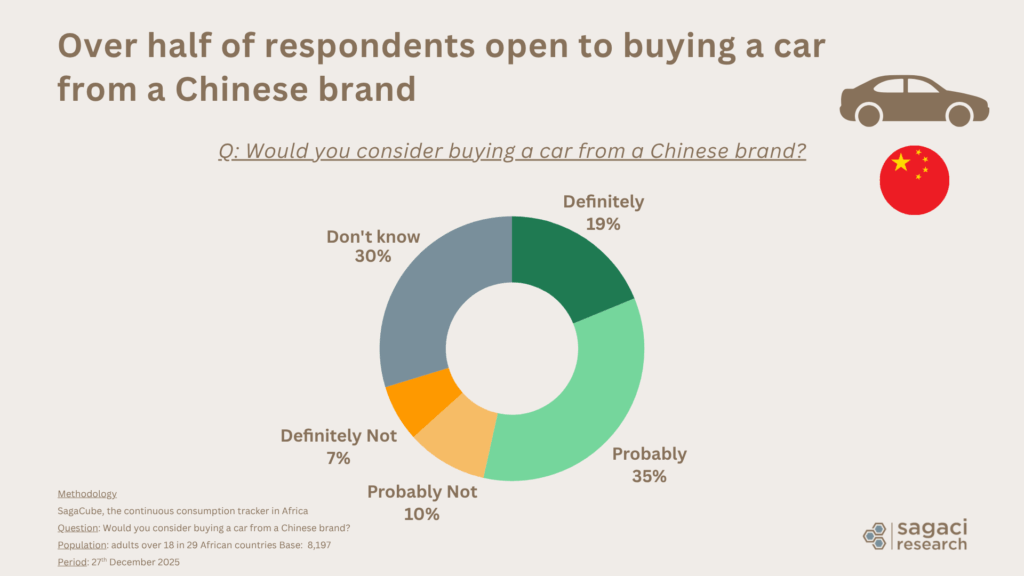

In last year’s article, Chinese brands were largely absent from the conversation. That is changing.

Our 2026 data shows that 54% of surveyed Africans say they would probably or definitely consider buying a car from a Chinese brand. Only 17% say probably not or definitely not. The remaining 30% say they don’t know, which reflects low familiarity rather than outright rejection and suggests significant room for awareness-building.

This openness is already translating into early ownership. Brands including Chery, BYD, Haval (Great Wall Motors), Jetour, JAC Motors, and Omoda & Jaecoo already appear in the ownership data. South Africa stands out as a key entry point for several of them.

For established brands, the strategic implication is clear. Price competitiveness is the most obvious lever Chinese manufacturers are pulling. But as quality perception improves and after-sales networks expand, their gains could come faster than expected. Markets like Egypt, Nigeria, and South Africa, which combine relatively high ownership rates with large consumer bases, are likely to be the primary battlegrounds.

The fuel shift: petrol today, hybrid tomorrow?

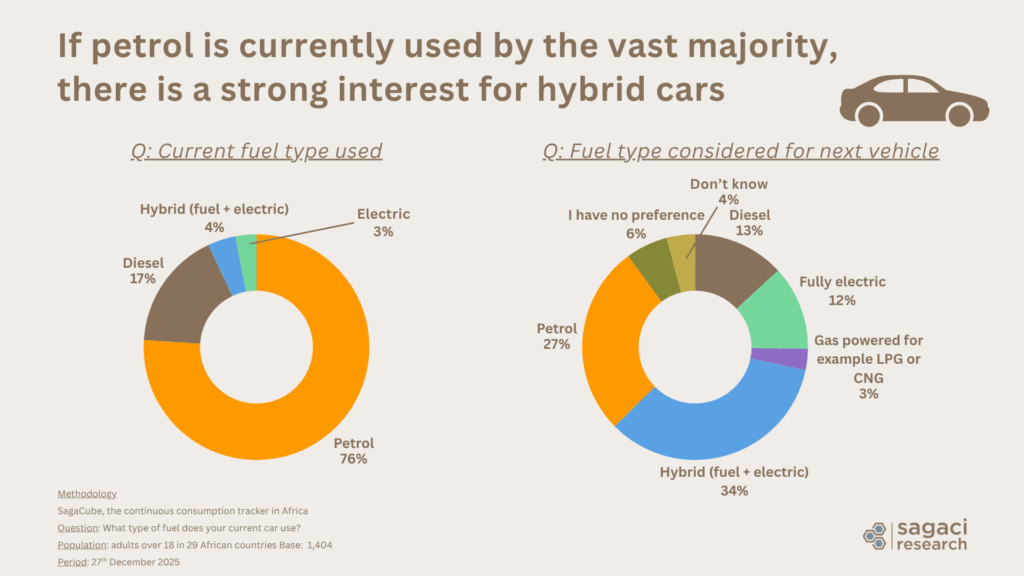

Africa’s current car park is overwhelmingly petrol-powered. According to our December 2025 data, 76% of car owners use petrol, 17% use diesel, and only 4% drive a hybrid vehicle, with electric cars at 3%.

But consumer intent for the next vehicle purchase tells a very different story. Hybrid (fuel and electric) is the most desired fuel type for next purchase at 34%, comfortably ahead of petrol at 27% and fully electric at 12%. Diesel drops to 13%.

This gap between current ownership and future intent is one of the most commercially significant findings in the report. It signals that African consumers are not resistant to cleaner technology. They are simply constrained by what is currently available and affordable in their markets.

Hybrid vehicles, which remove range anxiety and infrastructure dependency, represent the most realistic near-term opportunity for manufacturers looking to capture that intent.

For automotive players, the question is not whether Africa will shift away from petrol. The real race is about getting hybrid models to market at price points the continent’s middle segment can actually afford. The demand signal is already there.

The car market in Africa: what this means for the road ahead

Africa’s car market is at an inflection point. The fundamentals, low ownership rates, a predominantly second-hand market (75% of cars are bought used), and Toyota’s structural dominance across Sub-Saharan Africa, remain largely intact from what we reported a year ago.

But two new forces are gaining momentum:

- Chinese brands making a credible push for share

- A consumer base that is genuinely ready for hybrid vehicles when the product and price conditions are right

For manufacturers, dealers, and investors tracking Africa’s automotive sector, these are the trends worth watching closely in 2026 and beyond.

Sagaci Research tracks consumer behaviour across 30+ African markets continuously through SagaCube. For brand-level, country-level, or category-level automotive data, reach out to us at contact@sagaciresearch.com.

In the meantime, feel free to download the full report on the car market in Africa below.

Methodology

SagaCube, the continuous consumption tracker leveraging the largest online panel in Africa

Questions:

- Do you own a car?

- What type of fuel does your current car use?

- What fuel or energy type would you consider for your next vehicle?

- Did you buy your car… used, new, second-hand (…)?

- What is the brand of your car?

- Where did you buy the car you currently own?

- Would you consider buying a car from a Chinese brand?

Population: adults over 18 in 29 African countries Base: 8,199 (all) / 1,404 (car owners)

Period: 27th December 2025